OPINION

Market Rating Before FOMC MeetingJan 31

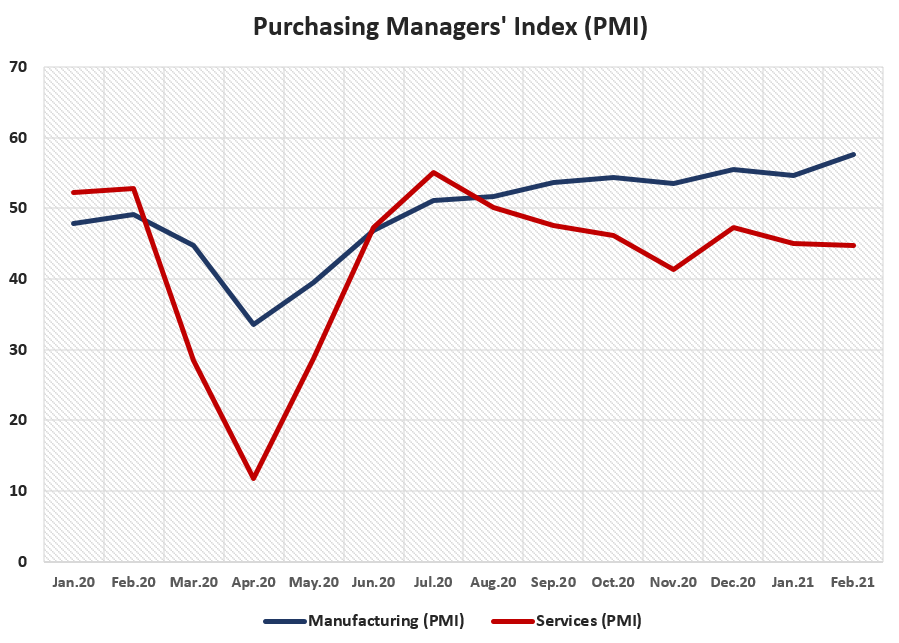

According to preliminary data announced for February by IHS Markit, a global information provider based in London; Service Purchasing Managers' Index (PMI) was registered as 44.7 points and remained below market expectations. Manufacturing Purchasing Managers' Index (PMI), on the other hand, was above expectations of 54.3, and recorded as 57.7 points.

The Eurozone countries had resorted to restraint measures from the last weeks of November in an attempt to take the outbreak under control. The restrictions were implemented in a way that did not do harm to the supply chain, yet the services couldn't perform well. Overshadowed by the measures, Services Purchasing Managers' Index continued its decline, while Manufacturing PMI data rose 2.9 points in February to 57.7, a 4-month peak.

The report published by IHS Markit stated that while the effects of measures taken against the outbreak were obvious in business activities and companies, it was less effective compared to the those in spring.

The implementation of the measures taken against the pandemic in a way that does not disrupt the supply chain caused a relatively downward outlook in January. However, Manufacturing PMI data rose in February because the tension in the supply of vaccines developed against the coronavirus pandemic ended. In addition, as part of measures taken to reduce the effects of the pandemic, unemployment rates increased in the Eurozone during the 12-month period, while the vast majority of these job losses were reportedly in the services sector.

The divergence in the sectors that make up the largest share of economic activity in the first quarter of the year indicates that the Eurozone will show a K shaped recovery in the first quarter. However, the possibility of reopening after lifting the restrictions related to the pandemic may pave the way for a recovery in the services sector after March, and this growth may accelerate in the second quarter.