OPINION

Market Rating Before FOMC MeetingJan 31

Financial markets are focused on today's nonfarm payrolls report as a key determinant of the Fed's monetary policy tightening momentum.

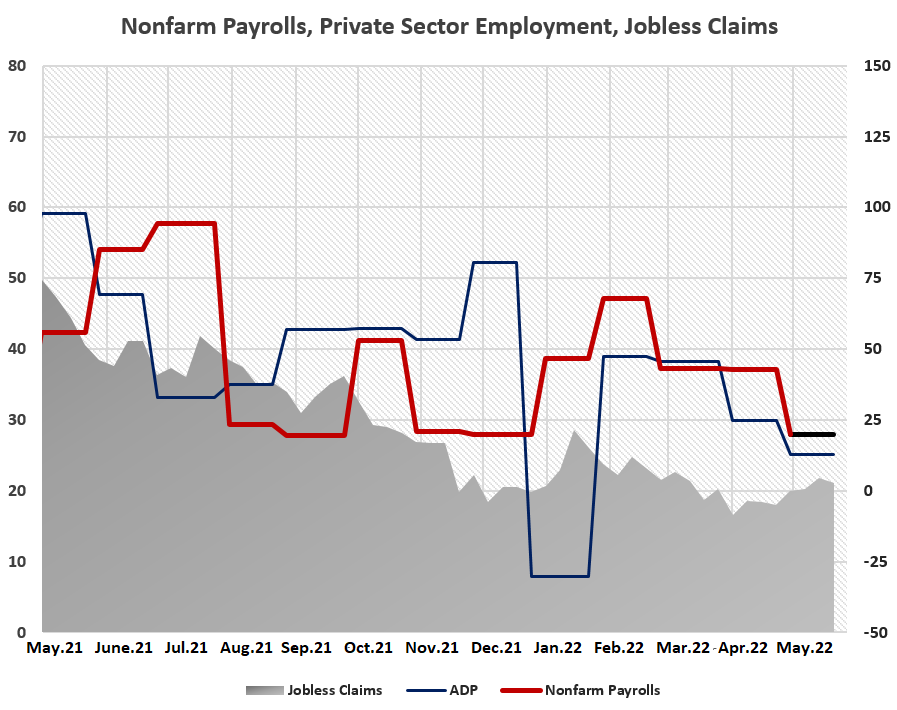

Estimates for the May labor statistics, which will be published by the Bureau of Labor Statistics (BoLS) of the US Department of Labor at 14:30 (GMT+2), are that the nonfarm payrolls will increase by 200 thousand. Chart-1: Nonfarm payrolls, ADP Private sector employment change and Jobless claims in the United States are divided by 10 thousand in the composite chart. The right axis of the charts shows nonfarm payrolls and ADP data, and the left axis shows the figure for jobless claims.

Chart-1: Nonfarm payrolls, ADP Private sector employment change and Jobless claims in the United States are divided by 10 thousand in the composite chart. The right axis of the charts shows nonfarm payrolls and ADP data, and the left axis shows the figure for jobless claims.

The Fed, which started monetary tightening in March for the first time since November 2018, made the largest-scale interest rate increase since 2000 with 50 basis points at its meeting on May 3-4, and pulled the federal funds target to the range of 0.75 - 1.00 percent. For Treasury securities, the cap will initially be set at $30 billion per month and after three months will increase to $60 billion per month. For agency debt and agency mortgage-backed securities, the cap will initially be set at $17.5 billion per month and after three months will increase to $35 billion per month.

While all participants agree that the labor market is extremely tight, the message that "more tightening than expected may be required" draws attention, bringing inflation to 2 percent as the long-term inflation outlook has increased over the period. It is also quite important that the authorities announce that they will continue to monitor the impact of incoming information on the economic outlook.

Under this view, it becomes clear that the Federal Open Market Committee (FOMC), relying on strong labor market conditions, wants to control inflation by putting the economy on a more balanced track. However, as Fed Chair Powell often repeats, wages that are increasing rapidly due to employers having difficulty finding workers will make an additional contribution to the inflation outlook,‘ putting great importance to labor stats.

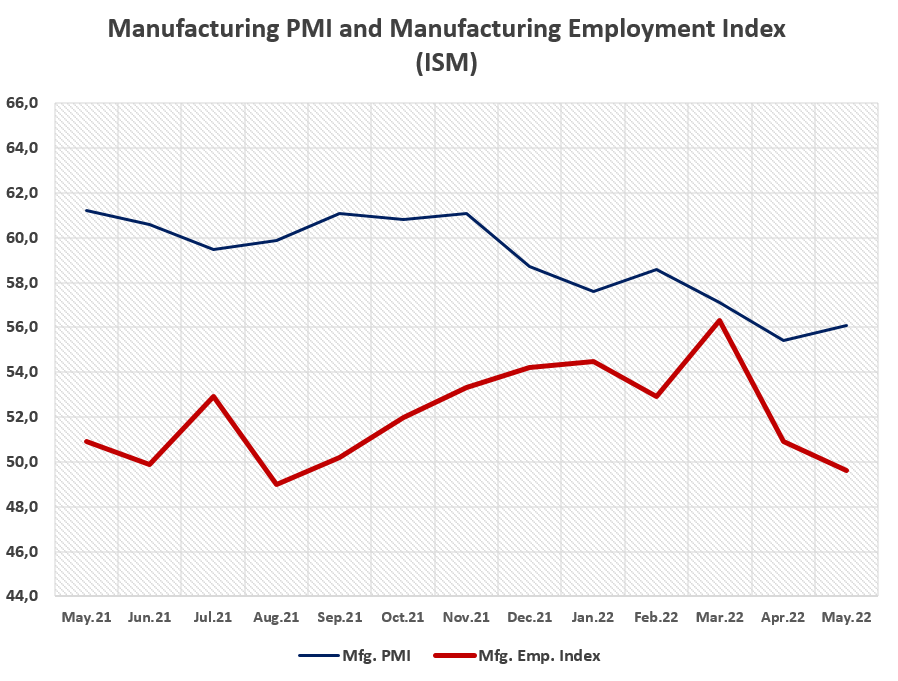

In the National Employment Report prepared in cooperation with ADP Research Institute and Moody's Analytics, the increase in private sector employment by 128 thousand in May is an important clue for nonfarm sectors. If we compare this with the performance of the locomotive sector of the US economy, as reported by the Institute of Supply Management (ISM), the manufacturing purchasing managers index (PMI) signals expansion despite the loss of momentum in May by 56.1 points, staying above market expectations.

On the other side, change in employment in the manufacturing sector is at its lowest level since August 2021 with 49.6 points. The uncertainty caused by the war, high commodity prices and the fact that the lockdowns in China, the largest trading partner of US companies, have reduced foreign demand and play a role as the main driver of manufacturing performance. Chart-2

Chart-2

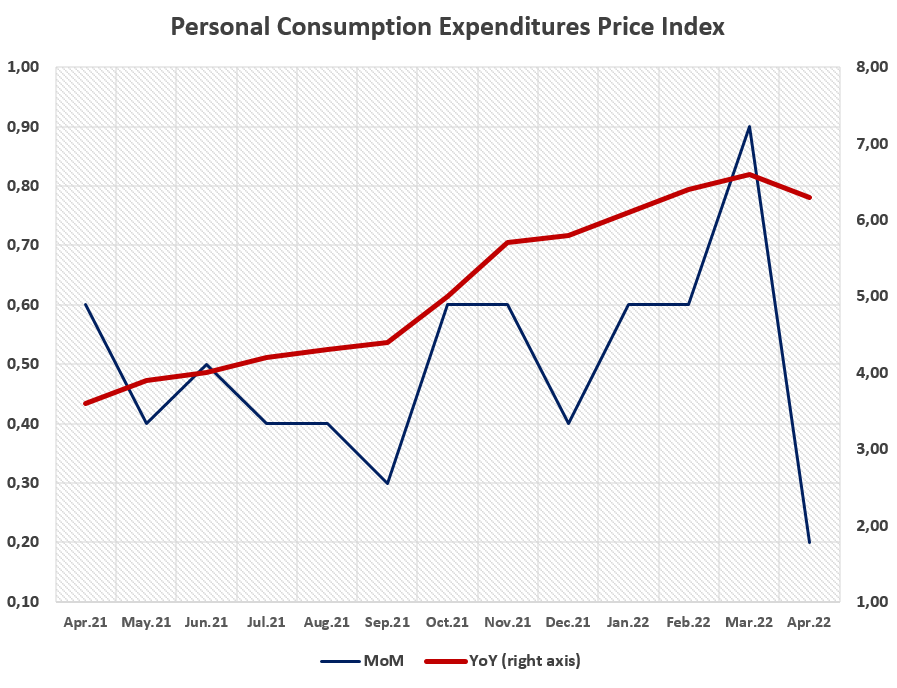

As a matter of fact, when Chart-1 and Chart-2 are compared, it seems that manufacturing employment and nonfarm payrolls are closely related. The recent decline in manufacturing mainly indicates that the nonfarm payrolls will not perform as it did in April. In other words, the contribution of the manufacturing sector to net employment is around minus 2.5 percent compared to the previous month.  Chart-3: In the chart, the monthly change for PCE is indicated on the left axis, while the annual rate of change is indicated on the right axis.

Chart-3: In the chart, the monthly change for PCE is indicated on the left axis, while the annual rate of change is indicated on the right axis.

On the other hand, the personal consumption expenditures price index (PCE deflator), known as the inflation indicator monitored by the Fed, increased by 0.2 percent in April and stood at 6.3 percent year-over-year. The deflator had risen by 6.6 percent the previous month, marking its biggest increase since 1982. This data relatively shows that the contribution of domestic demand to the growth of the domestic market is decreasing. However, it is still very clear that there is an inflationary pressure in the annual outlook. In addition, the decline in employment despite the growth in the manufacturing sector in May indicates that there may have been some increase in wages.

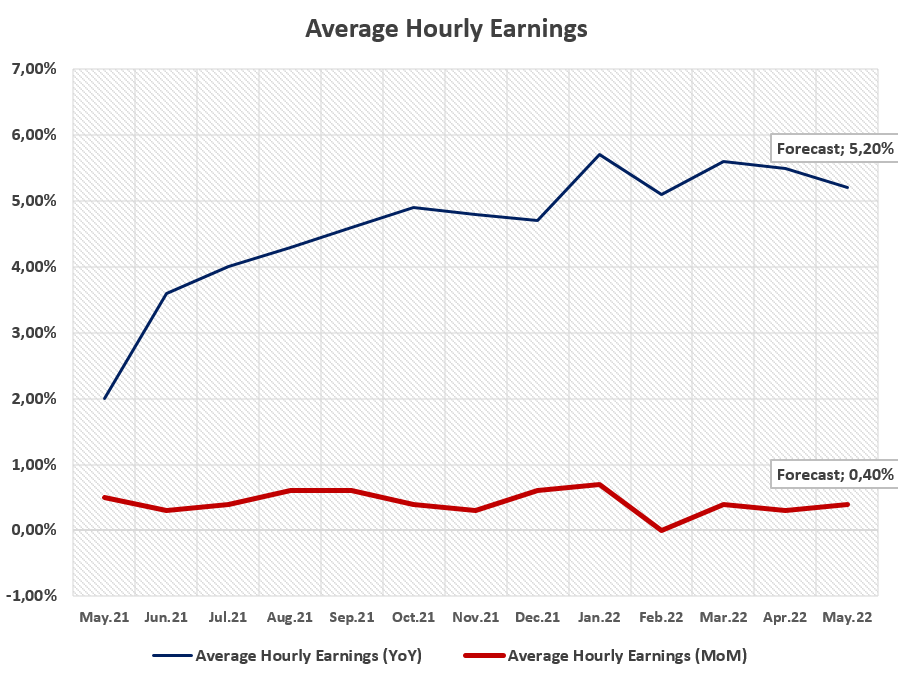

To sum up, nonfarm payrolls and average hourly earnings will be the main data releases that the markets will follow closely. If nonfarm payrolls stay below the forecasts of 200k and average hourly earnings are registered below 5.20 percent on annual basis, the downside effects of the Fed's monetary tightening process will prevail. By signaling that wage pressure has eased in parallel with the demand for labor, it may be expected that the bank will stop rate hikes following its meeting in July. On the other side, if nonfarm payrolls data exceeds 200k, it will show that labor conditions are tight. And in case, Average Hourly Earnings forecasts are also exceeded, US dollar may strengthen the pressure on relatively risk-sensitive assets due to the expectations that the Fed will increase the momentum of monetary tightening. Chart-4

Chart-4