Nonfarm Payrolls Report will indicate the Pressure on Inflation

International markets focused on the nonfarm payrolls report as an important determinant of the Federal Reserve's momentum to tighten monetary policy.

Bureau of Labor Statistics of US Department of Labor will release the data today at 14:00 (GMT+2) and nonfarm payrolls is expected to rise by 350k.

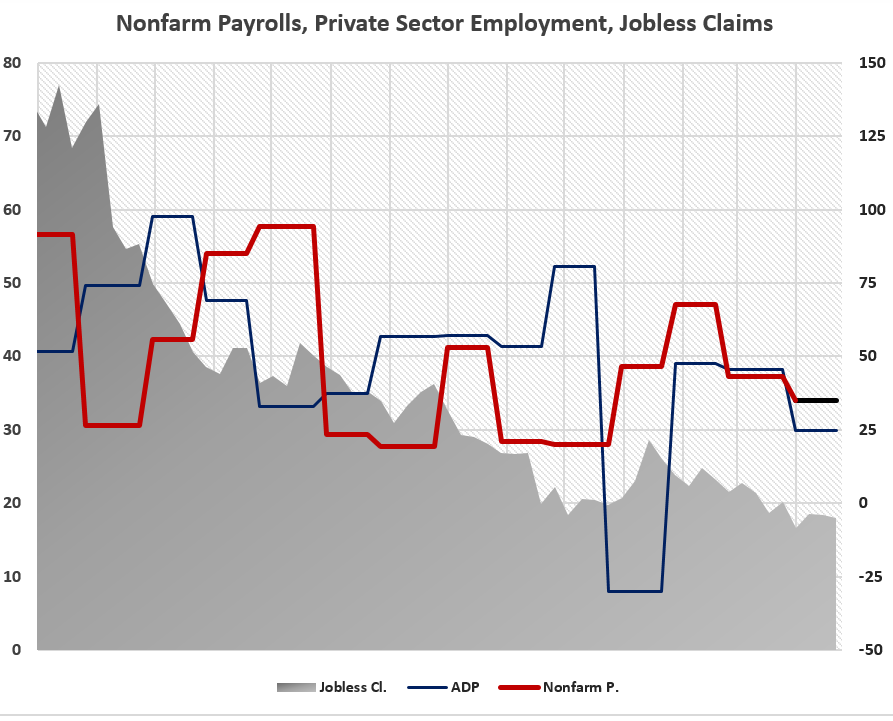

*Chart-1: Nonfarm payrolls, ADP Private sector employment change and Jobless claims in the United States are divided by 10 thousand in the composite chart. The right axis of the charts shows nonfarm payrolls and ADP data, and the left axis shows the figure for jobless claims.

The Fed, which is in a leading position on global monetary policy, has halted its ultra-loose monetary policy, which it introduced to support the labor market during the pandemic period, due to rising inflationary pressures. As Fed Chair Jerome Powell has often stated; wages, which are increasing rapidly due to the fact that employers are having difficulty finding workers in the extremely tight labor market, are an important element for the inflation outlook at this point.

The Fed, which increased interest rates for the first time since November 2018 at its March meeting, tightened its monetary policy by 50 basis points at its meeting on May 3-4, and pulled the federal funds target to the range of 0.75 - 1.00 percent. Thus, the Fed, which has realized its largest-scale monetary movement since 2000, informed that it will reduce its balance sheet of $ 8.94 trillion by $ 47.5 billion per month as of June 1 and by $ 60 billion per month after 3 months. Powell also noted that 50 basis point increase would be on the table at the next 2 meetings and that they would not hesitate to move the interest rate beyond the neutral level when needed.

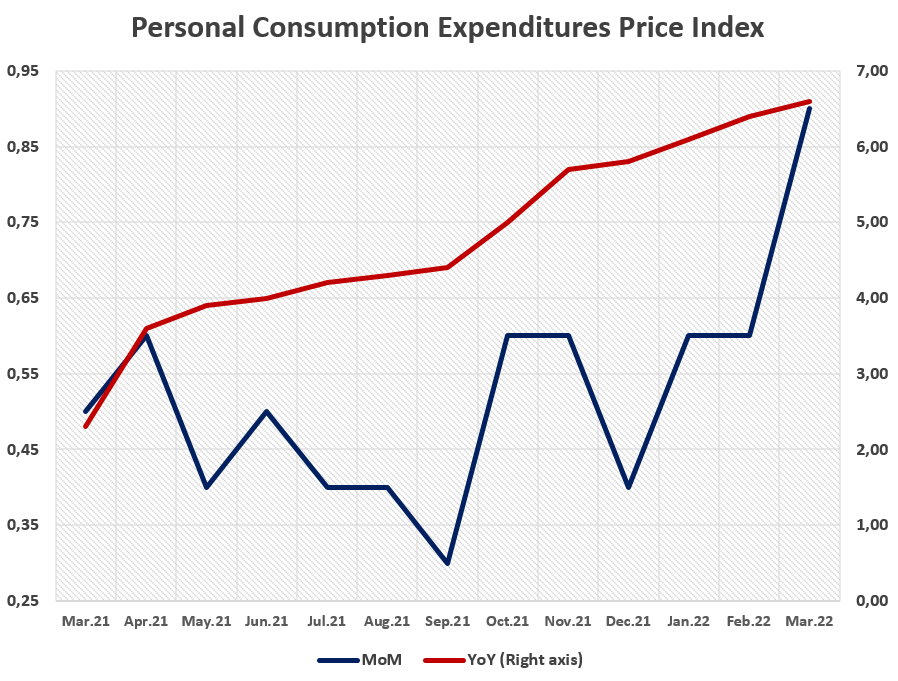

*Chart-2: In the composite chart, the monthly change for PCE is shown on the left axis and the annual change is shown on the right axis.

In March, Personal Consumption Expenditures price index (PCE deflator) increased by 0.9% (MOM) in March and this led to a 6.6% rise on annual basis, which was the largest increase since 1982. This is a sign that wages are creating a strong pressure on inflation.

On the other hand, it is quite clear that jobless claims fell in the face of conditions that indicate that frictional unemployment is on the way. The jobless claims announced by the Department of Labor were 200 thousand for the week ending on April 30. In the previous month, it was reported as 180 thousand. In other words, the pace of recovery is likely to lose momentum in the conditions of a tight labor market. In the National Employment Report prepared in cooperation with ADP Research Institute and Moody's Analytics, which is monitored as a preliminary data in the markets, the fact that private sector employment increased by 247 thousand in April also supports this.

However, it should be noted that the rising borrowing costs and changing expectations as a result of the monetary tightening that the Fed started in March, affected employers tendency to seek employees negatively. On the other hand, there is uncertainty caused by the Russia –Ukraine war and the impact of operating costs rising through the energy channel.

Chart-3

To sum up, labor market conditions in the world's largest economy are approaching full employment and thus, a slight loss of momentum in nonfarm payrolls can be considered reasonable. However, it is necessary to add that a level that may come well below the expectations of 350 thousand may also negatively affect the expectations for the economic outlook. Besides, in the labor statistics to be released, the average hourly earnings will be on the radar of the markets. Earnings were up by 0.4 percent MoM and 5.6 percent YoY in the March report. In the data set for April, average hourly earnings are expected to increase by 0.4 percent compared to the previous month and 5.5 percent compared to the same period last year.

Exceeding 6 percent on an annual basis may push the expectations for the FOMC meeting in June towards 75 basis points, revealing that the strong wage pressure on the headline inflation, which has been at the peak of 41 years in the US economy, will continue. The reflection of relatively high risk sensitivity on asset groups and the precious metal group may also be downward.