The U.S. Department of Labor's Bureau of Labor Statistics (BoLS) will release January labor force statistics at 15:30 (GMT+2) today.

Non-farm payrolls, which recorded an increase of 199 thousand in December, below the forecasts of 400 thousand, is expected to grow around 100 thousand in January, which is the lowest level in 12 months.

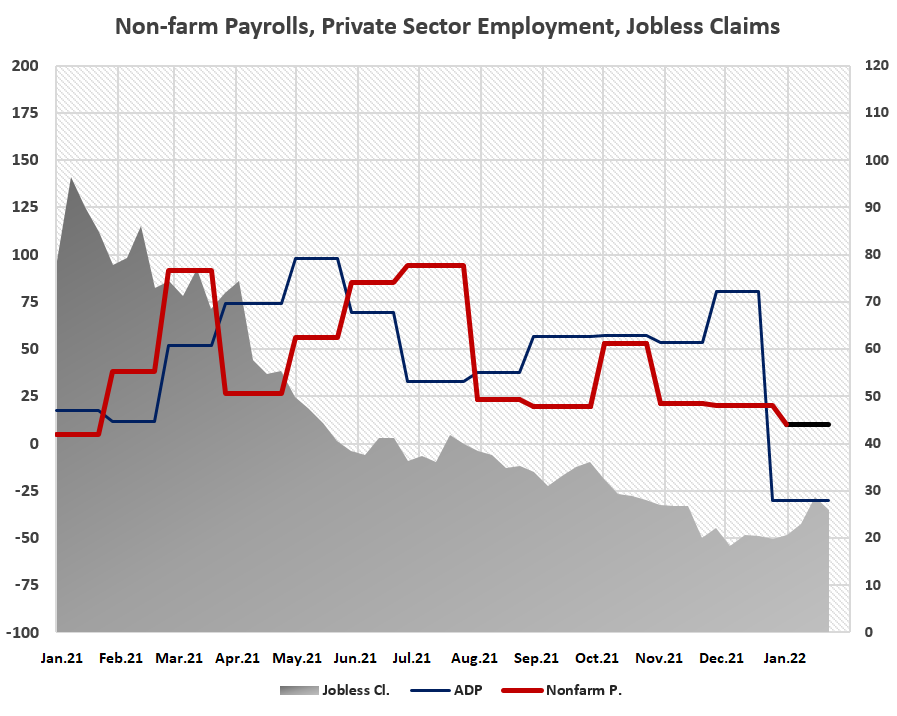

*Chart-1: Non-farm payrolls change, ADP private sector employment change, and the number of jobless claims are divided by 10,000 in the chart above. The left axis of the chart shows Non-farm payrolls and ADP data, and the right axis shows the number of jobless claims.

The employment report is of critical importance in terms of shaping the expectations of 25 to 50 basis points rate hike in the markets for the first interest rate hike, which will be on March according to the US Federal Reserve Chairman Jerome Powell’s comments following the Federal Open Market Committee (FOMC) meeting. The first non-farm payrolls data of the year will determine the expectations on when the Fed will start the balance sheet reduction process.

As a matter of fact, in the National Employment Report, which is accepted as a preliminary indicator, prepared by ADP Research Institute and Moody's Analytics, the decline in private sector employment by 301 thousand in January, despite the projections for an increase of 207 thousand, put a dent in the expectations for non-farm payrolls.

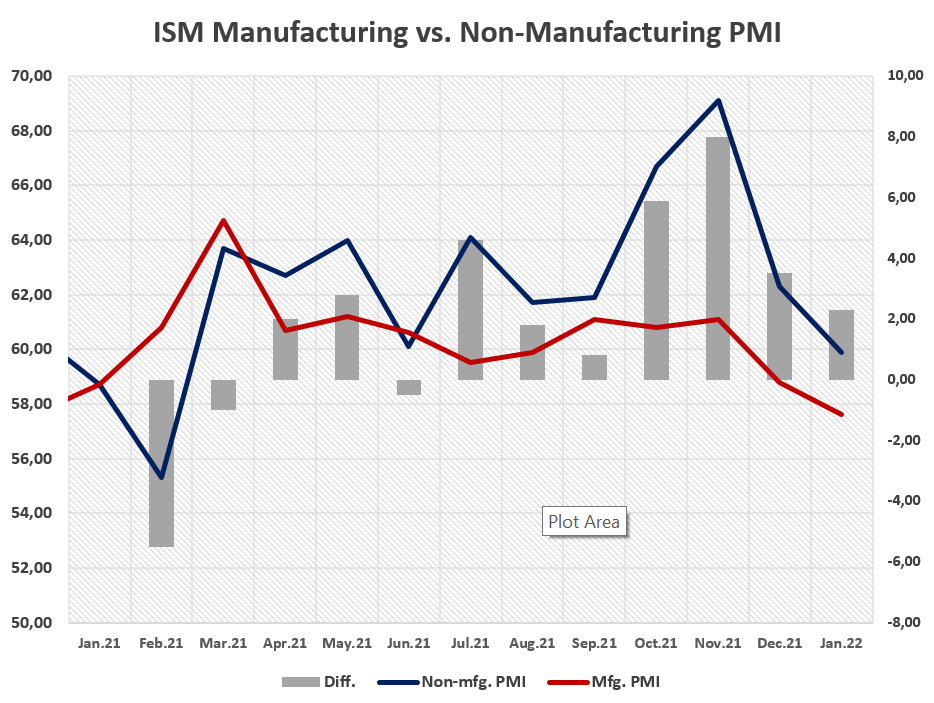

In January, manufacturing purchasing managers index (PMI) decreased by 1.87 percent to 57.6 and non-manufacturing purchasing managers index (PMI) also decreased by 3.5 percent to 59.9. So, taking the January data announced by the Institute for Supply Management (ISM) into account, we consider both PMIs as important intermediate factors.

PMI data indicate that the slowdown in growth observed in January in manufacturing and non-manufacturing (services, construction) activities, which are the locomotive sectors of the US economy, was transferred to the second month. In other words, the slowdown in growth in manufacturing and non-manufacturing activities shows that there is a recovery in the labor market, but it is progressing slowly.

*Chart-2: In the composite chart, manufacturing and non-manufacturing PMI indicators are shown on the left axis, and the difference in points are shown on the right axis.

We believe that the improvements due to the Omicron variant are still effective on the economy. The USA set a new record in the number of daily cases by exceeding 1.4 million. The 7-day average in case numbers left the plateau behind, yet it is still above 350 thousand as of the second half of January.

Although the high number of cases does not create a negative shock compared to the first period of the pandemic, it weakens the expectations on the job vacancies. Also, household spending may feel this pressure.

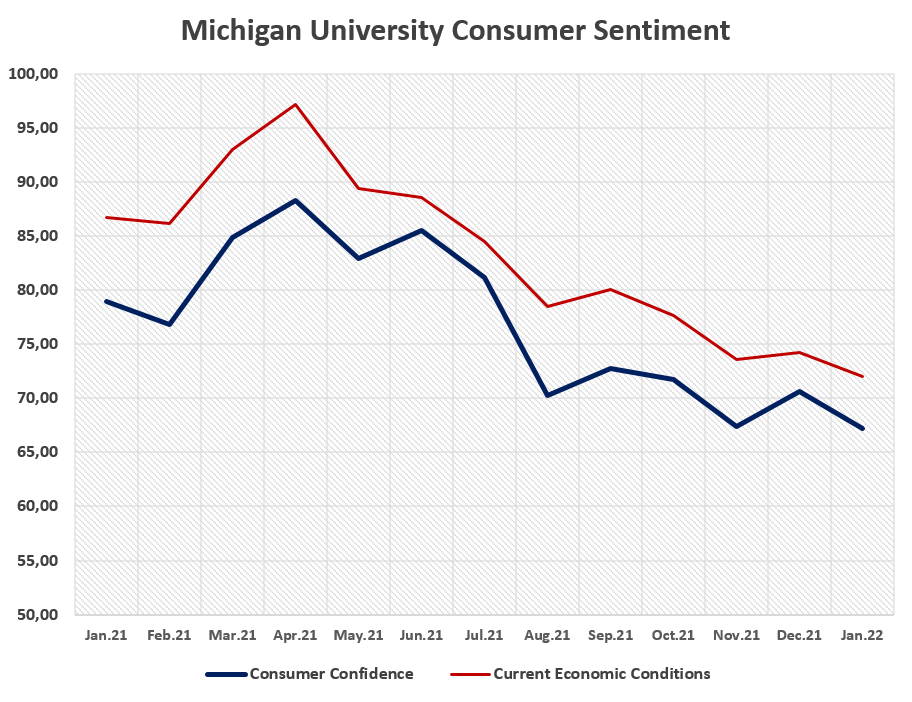

The results of the survey conducted by the University of Michigan Show that current economic conditions index declined by 2.9 percent to 72.0 points and consumer confidence also contracted by 4.8 percent to 67.2. After the strong recovery in the first half of 2021, indicators entered into a descending path, remarking that the pessimistic outlook continues to below the threshold value of 100.

To sum up, labor market progresses under strict conditions. However, rise in Covid-19 cases in January may affect the markets’ dynamics and lead to a cold slowdown in employment increase. Depending on the high-frequency data, which is close to that of January 2021, we estimate that non-farm payrolls will increase by around 100 thousand and the unemployment rate will converge to 3.8 percent in this period.

If non-farm payrolls are recorded above the forecast, it will confirm that the economy does not need an ultra-loose monetary policy support and expectations for the Fed's interest rate hike in March can be increased to 50 bps.

*Chart-1: Non-farm payrolls change, ADP private sector employment change, and the number of jobless claims are divided by 10,000 in the chart above. The left axis of the chart shows Non-farm payrolls and ADP data, and the right axis shows the number of jobless claims.

*Chart-1: Non-farm payrolls change, ADP private sector employment change, and the number of jobless claims are divided by 10,000 in the chart above. The left axis of the chart shows Non-farm payrolls and ADP data, and the right axis shows the number of jobless claims.  *Chart-2: In the composite chart, manufacturing and non-manufacturing PMI indicators are shown on the left axis, and the difference in points are shown on the right axis.

*Chart-2: In the composite chart, manufacturing and non-manufacturing PMI indicators are shown on the left axis, and the difference in points are shown on the right axis.