In his remarks to the Committee on Banking, Housing, and Urban Affairs, U.S. Senate, Federal Reserve Chair Jerome Powell said: "We will use our policy tools as appropriate to prevent higher inflation from becoming entrenched while promoting a sustainable expansion and a strong labor market." Following the implication for a rate hike by the Chair, market participants are focused on the 2nd non-farm payrolls release of 2022.

"Employers are having difficulties filling job openings, an unprecedented number of workers are quitting to take new jobs, and wages are rising at their fastest pace in many years," Powell also noted in his remarks. He further explained that reducing balance sheet will commence after the process of raising interest rates has begun. When the Federal Open Market Committee (FOMC) meeting on January 25-26 indicated March for monetary tightening, non-farm payrolls became critical in shaping the expectations of 25 or 50 basis points for the first rate hike in the markets.

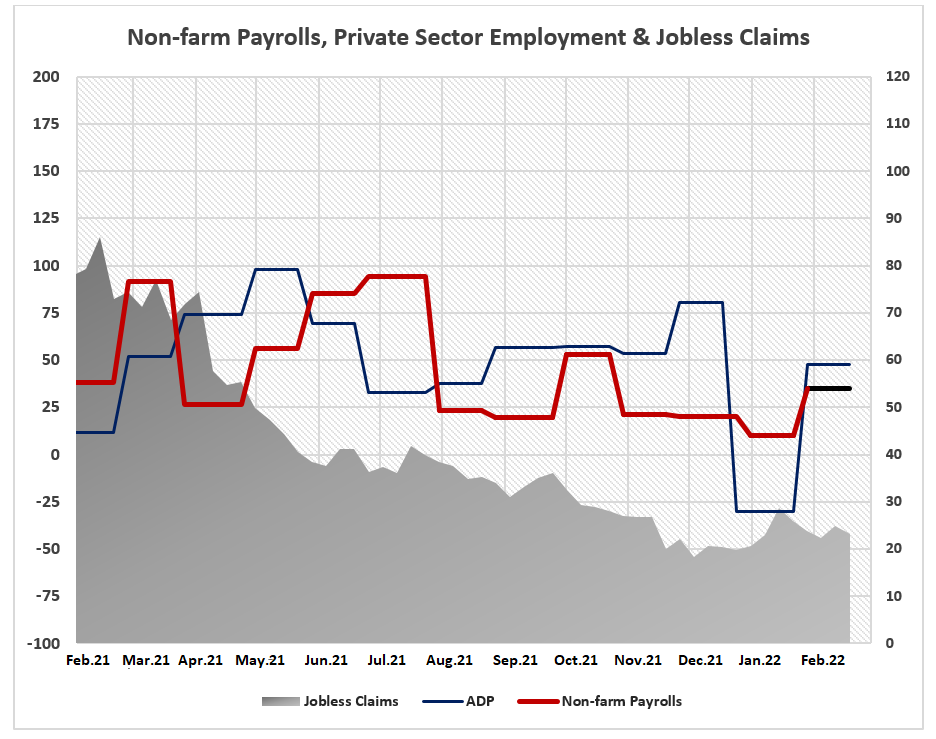

In the labor force statistics for February, which will be published by the Bureau of Labor Statistics (BoLS) of the US Department of Labor at 15:30 (GMT+2) today, non-farm payrolls are expected to be around 350 thousand. In January, the payrolls had tripled the forecasts of 150 thousand and registered as 467 thousand.

*Chart-1: Non-farm payrolls change, ADP private sector employment change, and the number of jobless claims are divided by 10,000 in the chart above. The left axis of the chart shows Non-farm payrolls and ADP data, and the right axis shows the number of jobless claims.

In the National Employment Report prepared in cooperation with ADP Research Institute and Moody's Analytics, which is considered to be the leading indicator of the labor market in the world's largest economy, private sector employment increased by 475 thousand in February.

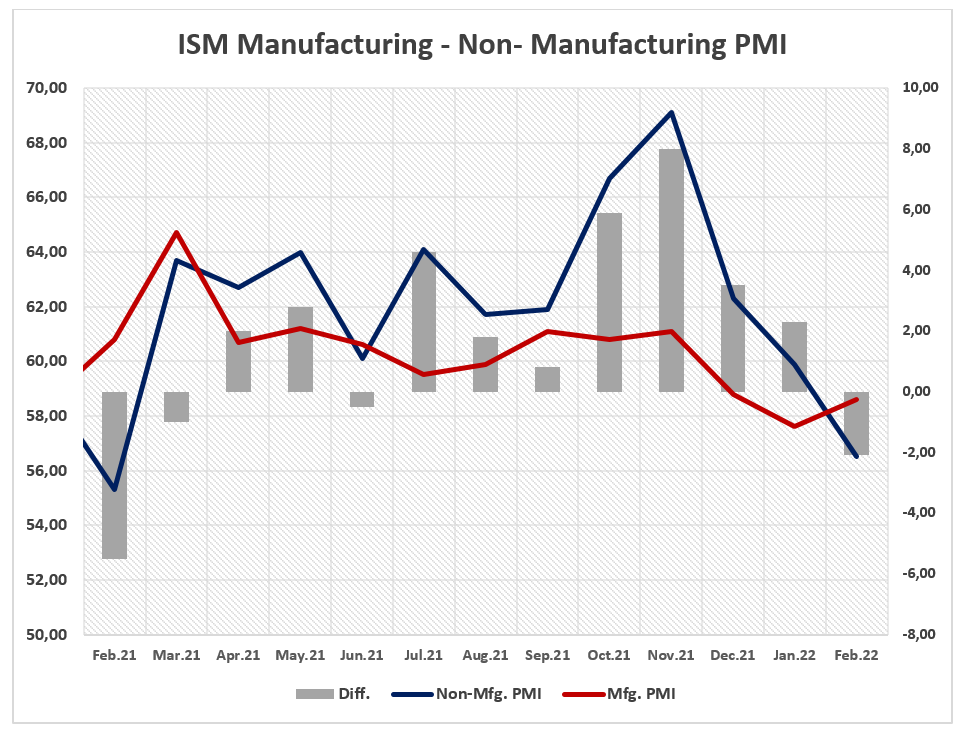

At this point, the data of the Institute for Supply Management (ISM) can be taken into account while seeking the contribution to private sector employment. According to ISM, manufacturing purchasing managers' index (PMI) in the United States increased by 1.7 percent to 58.6 points in February, while non-manufacturing purchasing managers' index (PMI) fell by 5.6 percent to 56.5.

Chart - 2 shows that recovery in manufacturing in February significantly contributed to the labor market. The chart also indicates the expansion in manufacturing exceeded that of non-manufacturing (service, construction) sector. Although non-manufacturing PMI indicates growth above the threshold value of 50, it is very clear that the pace of expansion is decreasing.

*Chart - 2: In the composite chart, the manufacturing and non-manufacturing PMI indicators are shown on the left axis, and their differences in points are shown on the right axis.

As Powell pointed out vacant job positions are prominent; however, the impact of coronavirus case numbers and the Russia –Ukraine war, which is a global crisis now, are also big questions. Due to the war in Ukraine, oil prices exceeded the highest level of the last 8 years and created an additional cost pressure for US businesses. In addition, although the case numbers are not a big concern anymore when compared to the first period of the pandemic, it weakens employers' projections and expectations. Starting February with a daily number of cases of about 660 thousand, the United States reported 107,799 cases as of February 28 and the 7-day average is at 72,730.

Chart-3

Looking at the results of the surveys conducted by the University of Michigan, current economic conditions index declined by 5.2 to 68.2 and index of consumer sentiment also fell by 6.5 to 62.8 and showed that net contribution to the service sector declined significantly.

To sum up, in the face of manufacturing sector performance, we assess that the relatively moderate coronavirus case numbers in February will have some negative impact on service sector expansion, but its impact on resilient economic activity will be limited. However, the increase in labor demand may not be strong due to the inflationary setting caused by high energy costs. Thus, Federal Reserve's rate hike expectations are likely to reach 50 basis points in order to combat high inflation in a tight labor market, in case, non-farm payrolls exceed the forecast of 350 thousand in February. On the other side, if the data stays below 350 thousand, the Fed is likely to continue to encourage the labor market and clarify its expectations that it will increase interest rates by 25 basis points to prevent inflation from becoming permanent.